Consumer Alert: Protecting Your Cash and Credit in College. Part 4: How student loans and credit card debt affect your credit score.

[anvplayer video=”5039596″ station=”998131″]

ROCHESTER, N.Y. (WHEC) — All this week, I’ve been alerting you to ways to protect your cash and credit in college. As the parent of a soon-to-be college kid, I want to share with you everything I wish I knew before I was sent off into the wild blue yonder.

Now, we’re taking a look at student loan debt versus credit card debt. I discussed how student loan debt can affect your credit score with Rod Griffin, the Senior Director of Consumer Education and Advocacy at Experian.

"It [a student loan] can have a huge impact both positive and negative," Griffin said. "So, if you’re paying a student loan, it’s just like have a car loan or a mortgage. So paying it on time will show that you’re responsible for that debt. It will build a positive payment history and will boost your credit scores over time. If you fail to pay that loan, it’s going to have the same effect it would if you didn’t pay your car loan."

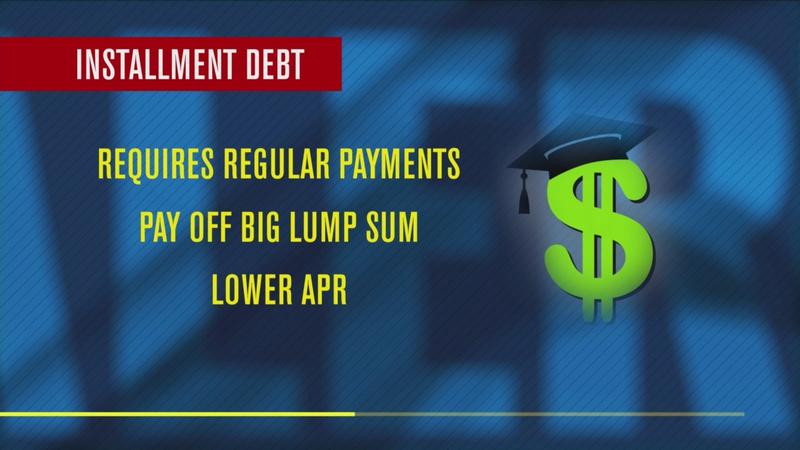

Student loan debt is installment debt, something on which you make regular payments like your car and your mortgage. You borrow a big lump sum in the beginning and pay it off over time. The APR is usually much lower than credit card debt. Right now, the interest rate for student loan debt is 2.75%.

[News10NBC]

Compare that to credit card debt which is revolving debt. You have a credit limit and can keep borrowing until you reach it. The APR is much higher than the installment debt. Right now the average credit card APR is 16.61%. It’s a good practice to use a credit card calculator to see the real cost of credit card debt. Revolving debt has the greatest impact on your credit score. That’s because your credit card debt factors into your credit utilization. It looks at the amount of credit available to you versus the amount of debt.

So, if you’re trying to improve your credit score, the best rule of thumb is to pay off your credit cards first. But you can’t skip your student loan payments. If you’re having trouble paying your federal student loans, there are several options, like deferment or forbearance, which allow you to postpone student loan payments when you can’t afford them.

Federal loans also have other programs that can reduce your debt. These programs are not available if you got a private student loan.

The key is building a credit history in college without accumulating debt. I addressed how to do that in Monday’s consumer alert.

If you begin building good credit in college, all those dreams you hope to achieve after college are far more likely to be within reach.